Australia's surcharge rules are changing

Here's what that means for our software platforms and merchants.

Updated on 30th June 2026

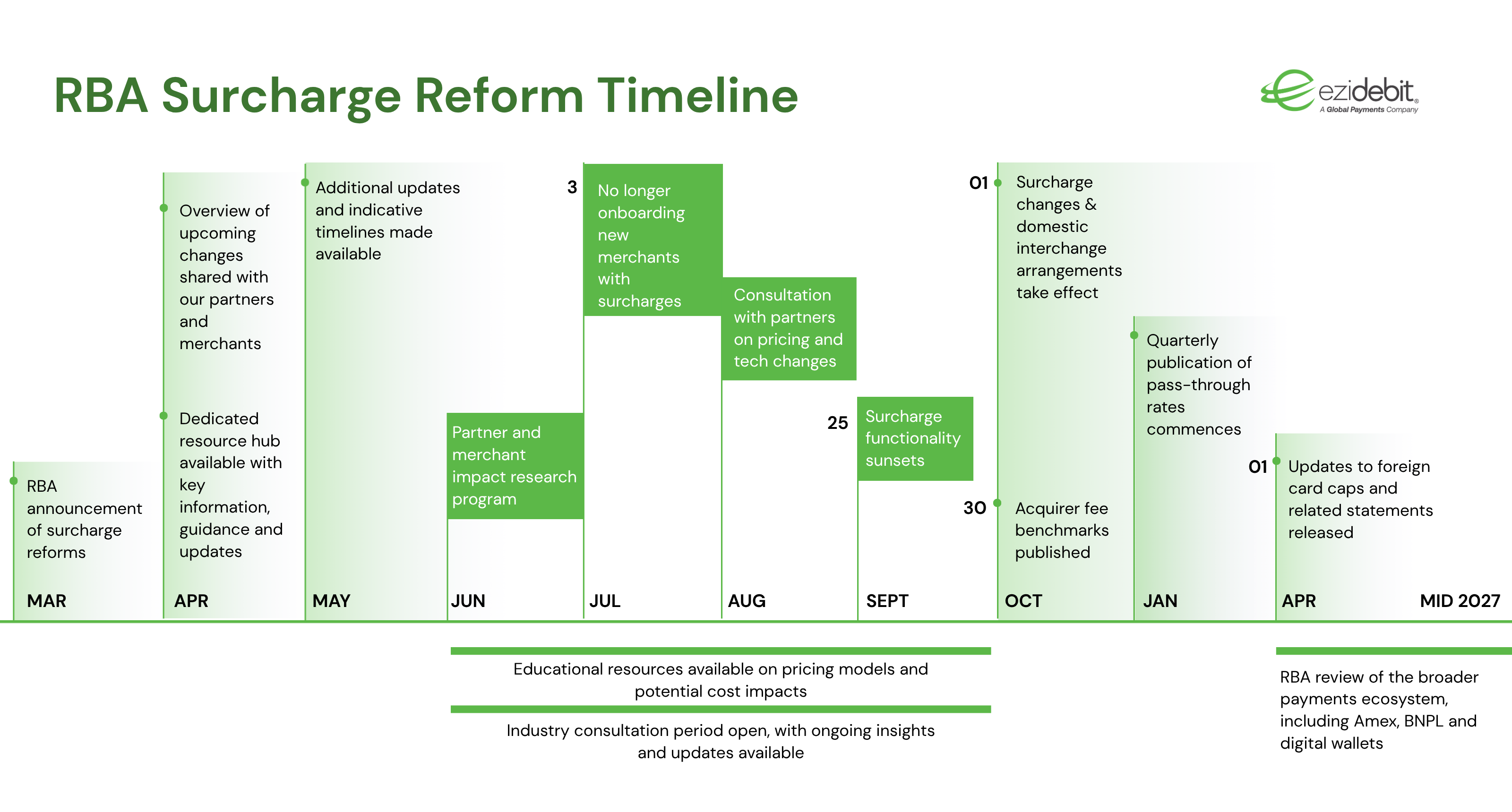

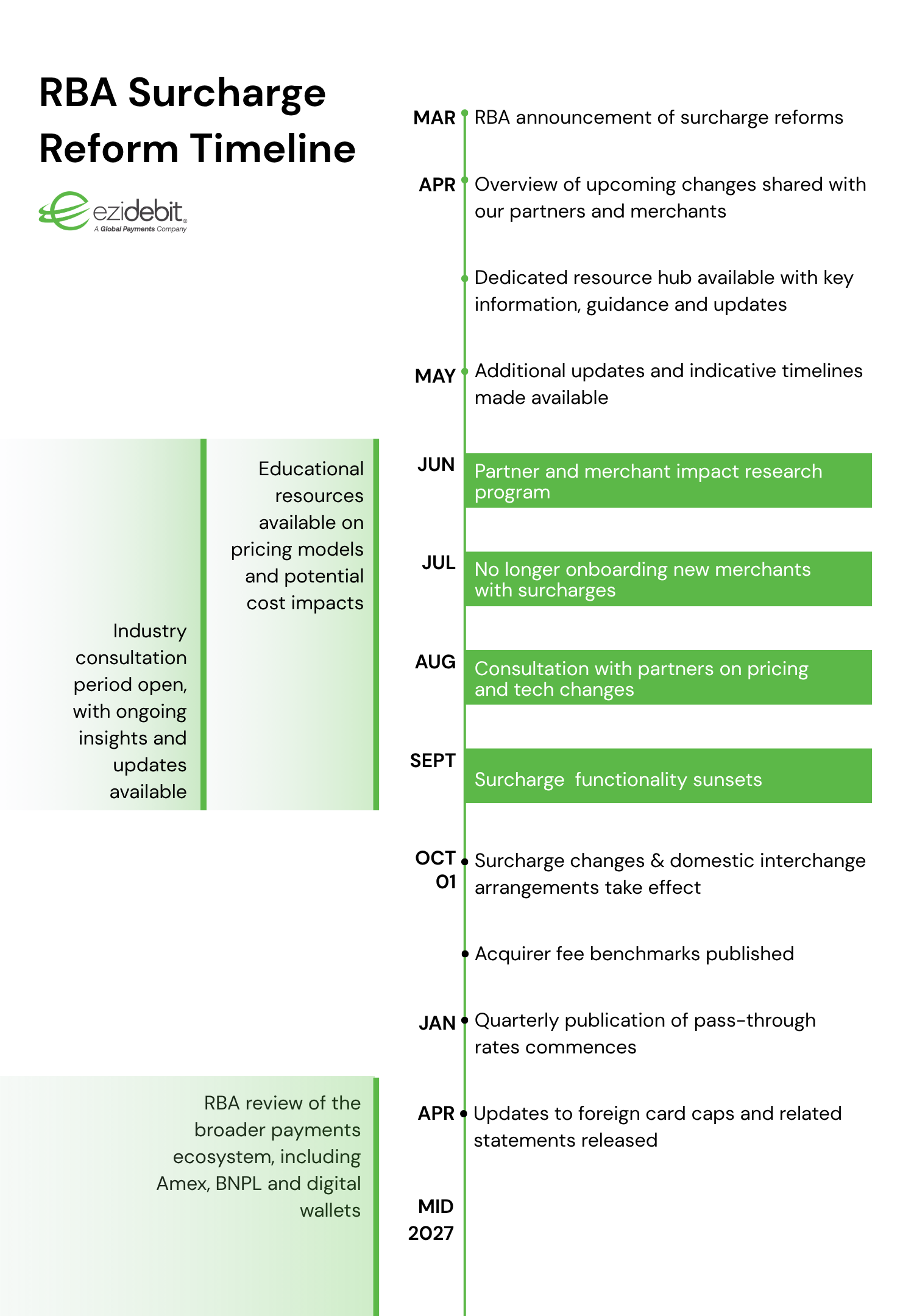

The Reserve Bank of Australia (RBA) has finalised reforms to card payment surcharging and interchange fees, effective 1 October 2026. As your payments partner, we're committed to making this transition straightforward for your business. We are currently in the planning and preparation phase, working closely across teams to ensure everything is in place for a smooth transition for our partners and customers.